Will CBDCs Replace Banks - or Just Force them to Evolve?

1. Finance Students Are Entering a Changed Monetary Landscape

If you're a finance student today, you're preparing to enter an industry that is about to experience one of the biggest structural shifts since the invention of electronic banking. Central bank digital currencies (CBDCs) are no longer abstract concepts discussed in monetary policy courses—they’re being tested by major institutions like the European Central Bank, Federal Reserve, and People’s Bank of China.

What started as a reaction to crypto has become a real attempt to redesign how money itself works.

This leaves you—and future employers in banking, fintech, and investment—with a critical question:

If people can hold risk-free digital money directly at the central bank, what happens to commercial banks?

Let’s break it down.

2. What Exactly Is a CBDC? (And Why Should Finance Majors Care?)

Images by exp.science

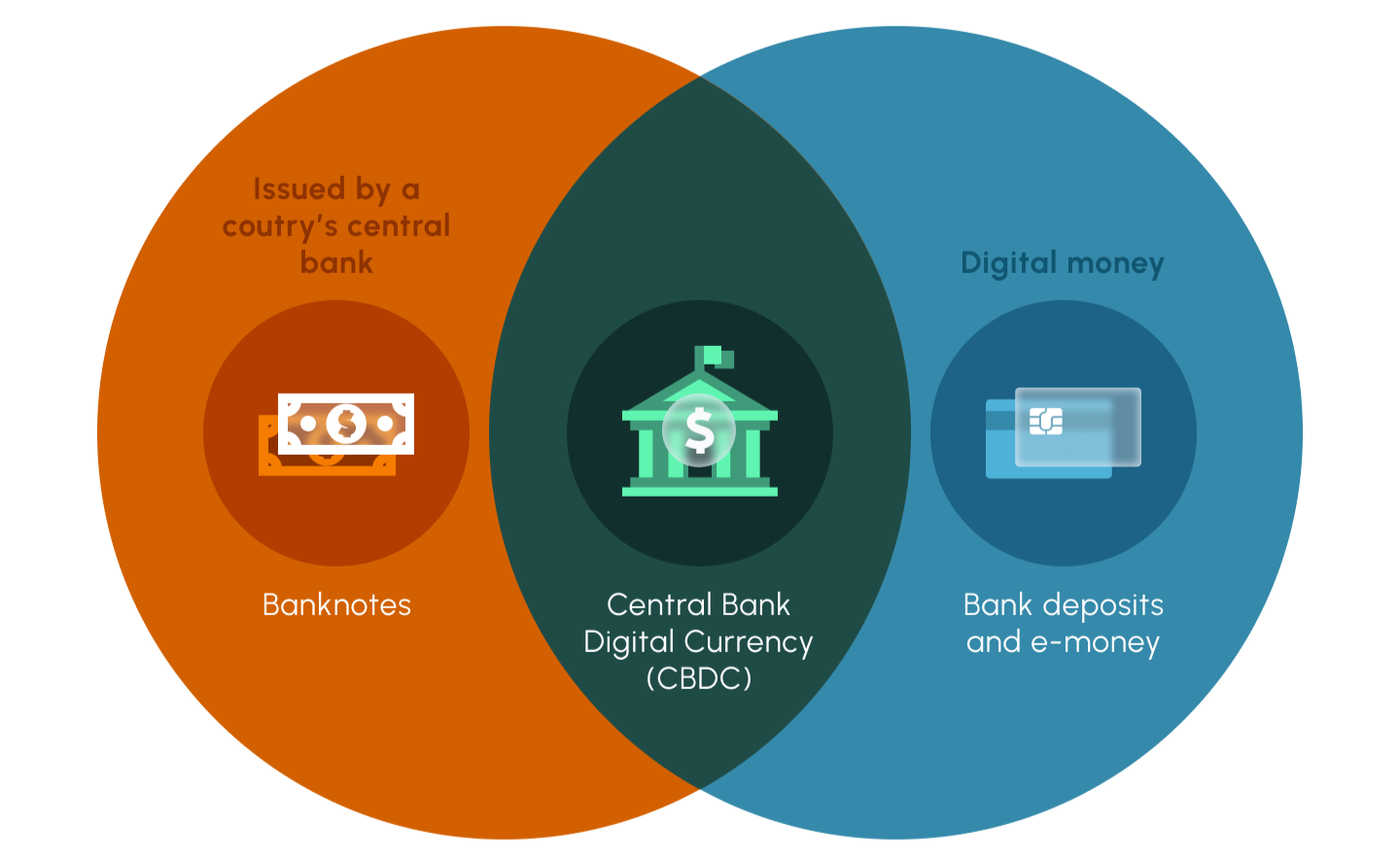

A CBDC is digital cash issued by the central bank.

Not a cryptocurrency.

Not a stablecoin.

Not a private app like PayPal.

Today, when you log into your bank account, your balance is a claim on a commercial bank. A CBDC would make your balance a direct claim on the central bank, like physical cash—but digital.

For finance students, this matters because it challenges the business model you’ve been studying:

Banks collect deposits -> Banks make loans -> Banks earn interest spreads.

CBDCs interrupt step one.

3. Deposit Flight: The Biggest Fear for Commercial Banks

Commercial banks rely on deposits as their cheapest funding source. CBDCs give consumers a safer alternative—direct central bank money.

Research You Should Know:

Economists at the Bank of Italy found that CBDCs could drain deposits from commercial banks and force them to replace that funding with costlier borrowing—unless CBDCs have limits or disincentives.

This is a major exam-style point if you study:

· Financial institutions

· Banking management

· Monetary policy

· Risk and regulation

CBDCs don’t automatically destabilize banks—but poor design can.

4. Risk Redistribution: A New Financial Architecture

A major question finance students should ask is:

If money leaves banks, who absorbs the credit risk?

If consumers shift money out of banks and into CBDCs, central banks might need to lend money back to banks to keep credit flowing. But that flips the traditional risk structure on its head. A 2024 article in the Statistics Swiss Journal of Economics and Statistics argues that issuing a retail CBDC could shift credit risk from private banks to central banks.

In other words, CBDCs don’t just redistribute deposits—they redistribute risk.

This means that if banks start losing deposits, central banks may end up directly financing lending activity. That’s a role they’ve never held at scale, and it blurs the line between monetary policy and commercial banking.

5. Global Differences: Why Finance Students Must Think Internationally

CBDC impacts are not uniform.

A study published in FinTech using a GVAR model found that emerging markets (Brazil, India) experience greater instability when CBDCs enter the system than advanced economies (Japan, UK). Many developing countries rely more heavily on cash and fragile deposit bases.

For students interested in:

· International finance

· Global markets

· Development economics

CBDCs may widen the gap between strong and weak banking systems.

6. Will CBDCs Kill Banks? Probably Not - But They’ll Change Your Future Job

Most central banks—including the ECB—support a two-tier model, where:

· The central bank issues the CBDC

· Commercial banks handle customers, compliance, onboarding, and services

That means banks won’t disappear.

They’ll pivot.

What commercial banking may look like when you graduate:

✔ More focus on lending and credit expertise

✔ More advisory, wealth management, and relationship roles

✔ Greater collaboration with fintech and digital payment platforms

✔ Less dependence on deposit-based funding

Banks will become service providers, not just deposit warehouses.

For students considering careers in commercial banking or fintech, this shift can create more opportunities—especially in digital payments, financial data analysis, compliance, and CBDC-related policy roles.

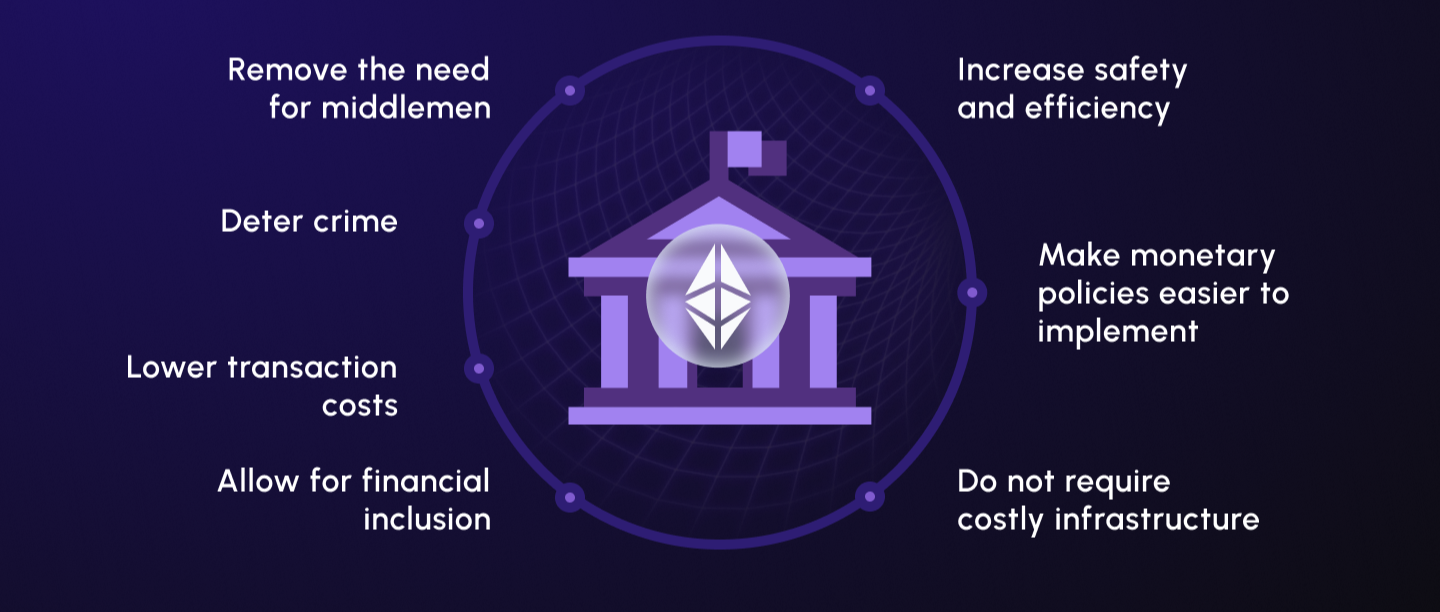

7. A Strategic Purpose: Stability, Sovereignty, and the Future System

CBDCs are not just a response to crypto—they’re a strategic move.

G7 policymakers argue CBDCs will:

· enhance financial stability

· defend monetary sovereignty

· prevent Big Tech and private tokens from dominating payments

· reduce energy consumption compared to crypto mining

This means CBDCs aren’t designed to destroy banks—they’re designed to modernize the monetary system.

8. Why Finance Students Should Pay Attention

As a finance student, CBDCs are not just a topic in a lecture—they’re a blueprint for the system you’ll be working in.

CBDCs will:

· change how banks fund themselves

· reshape credit markets

· force new liquidity and risk models

· alter global financial stability

· create new digital-finance roles

But they won’t eliminate banks.

They will force banks to evolve—and your career will evolve along with them.

Understanding CBDCs today gives you a competitive edge tomorrow.